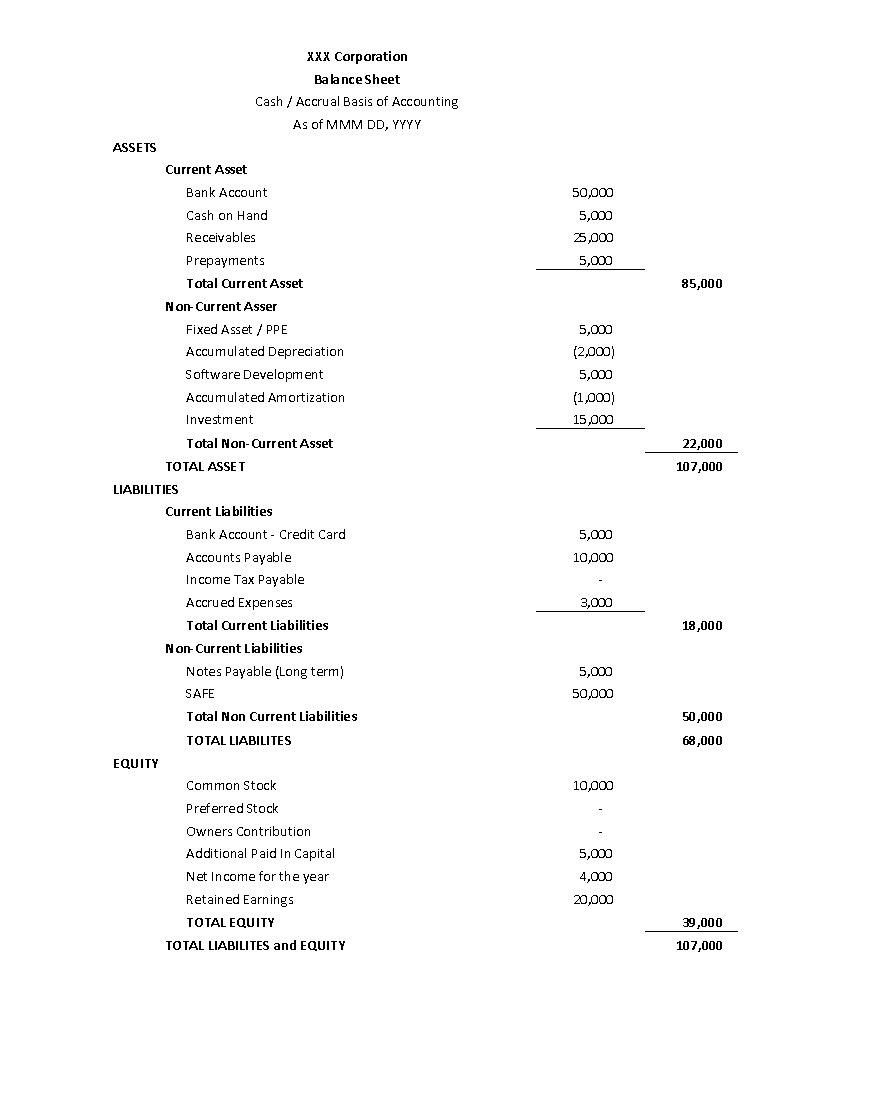

A balance sheet is a financial statement that shows a company’s resources (assets) and how they were financed at a given time period, either through debt (liabilities) or equity contributions from owners/shareholders. It is also known as the Statement of Financial Position.

It can be implied with this structure: Asset = Liabilities + Equity

Why is the Balance Sheet Important?

A balance sheet shows a company’s financial position over a certain period. It provides data that can be useful in tracking the performance of the business.

What are the Benefits of the Balance Sheet? Who uses a Balance Sheet?

To Owners:

- It provides a snapshot of the company’s finances. It shows the company’s assets (cash, receivables, and prepayments) and liabilities (debt). It also displays the cumulative Income/ Loss and the contributions of the owner/ investors.

To Investors/Shareholders:

- It explains where their money will go, whether it will be spent on operations or used to pay off the company’s debt. It will also provide a summary of the company’s finances at a specific point in time.

- Future investors can use this report to decide whether or not to invest, as it shows the company’s financial health and how it operates.

To Tax Preparers:

- It appears on Schedule L of a C corporation’s tax return.

Other Uses of the Balance Sheet

- It can immediately determine whether your assets can cover your liabilities.

- In the event of dissolution, it provides information about how much stockholders/owners can retain after paying all of their liabilities.

- It also influences the decision to distribute dividends to stockholders.

- If assets exceed liabilities, the company’s financial health improves because assets add value to the business.

What Type of Companies Does This Apply To?

The balance sheet is applicable to all companies; the only difference is the chart of accounts used. As companies are in different industries, for example, a manufacturing company may use accounts like packaging costs while a service company does not.

Read More: Understanding the Cash Flow Statement: An Overview of Key Concepts

Definition of each term appearing in the balance sheet

NOTE: Accounts Receivable, payables (accounts and notes), prepayments, and Accrued expenses are only applicable to the accrual basis of accounting.